Appraisals, Underwriting & the Waiting Game | The Buyer’s Reality Check Series

Financing Phase

Progress is not always visible.

After the option period ends, many buyers expect the transaction to feel like it is moving faster. Instead, this phase often becomes quieter—sometimes uncomfortably so.

Documents are submitted. Questions come in waves. Then there may be stretches of silence.

That silence does not mean nothing is happening. It often means verification is underway.

This stage focuses on confirming two things:

- The home’s value (appraisal)

- The buyer’s financial profile (underwriting)

It’s procedural, not emotional—which is why it feels slower than earlier phases.

The Appraisal

The appraisal is used to confirm that the home’s value supports the loan amount. It is not a judgment about whether the buyer chose well. It is a data-based assessment that considers comparable sales, property features, and condition.

When the appraisal supports the contract price, the process continues forward. When it does not, it creates a new conversation around options—not an automatic failure.

Underwriting

Underwriting is the lender’s process for verifying income, assets, credit, and supporting documentation. Requests can feel repetitive or poorly timed because the file is often reviewed in layers, with different items surfacing at different points.

Silence during this stage is common. In many cases, it simply means the file is being reviewed and worked behind the scenes.

Why This Phase Feels Stressful

Buyers are no longer making many active decisions—they are waiting for other professionals to complete their reviews. That loss of visibility can create concern, even when the transaction is moving forward normally.

In this phase, no news is often simply that: no new issue to report.

Progress in this phase is mostly happening behind the scenes:

- Reviews are completed carefully

- Conditions are cleared methodically

- Timelines are monitored closely

This stage is about building certainty, not creating speed.

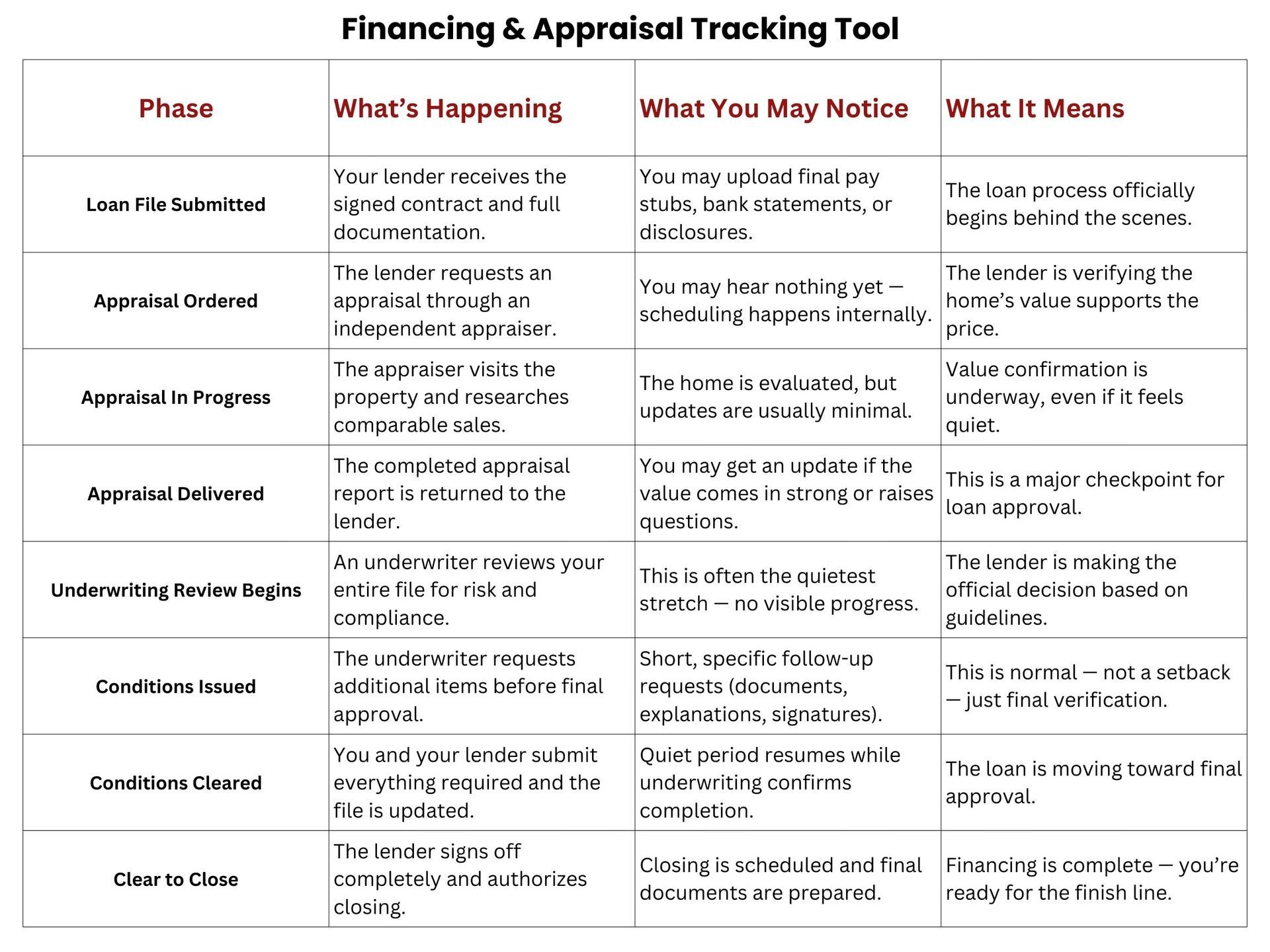

The Financing & Appraisal Tracking Tool helps buyers understand where they are in the process so waiting does not turn into unnecessary worry. It provides a clearer view of key milestones, helping buyers recognize that progress is still being made even when updates feel less frequent.

During this phase, Cindy Coggins Realty Group remains involved—monitoring timelines, staying attentive to communication, and helping keep the transaction moving forward.

Frequently Asked Questions About Appraisals and Underwriting

When does the appraisal usually happen during the buying process?

The appraisal is usually ordered after the buyer is under contract and the lender has the loan file moving forward. Timing can vary based on the lender, appraiser availability, property type, and closing timeline.

Who orders the appraisal?

The lender typically orders the appraisal through an approved appraisal process. The buyer usually pays for it as part of the loan process, but the appraiser is not chosen directly by the buyer, seller, or real estate agent.

Can a buyer attend the appraisal?

Most buyers do not attend the appraisal. The appraiser usually schedules access to the property and completes the evaluation independently. In some cases, the listing agent may provide helpful property information or comparable sales data.

What happens if the appraisal comes in lower than the contract price?

A low appraisal may create several possible paths, depending on the contract, loan type, buyer’s available funds, seller’s position, and negotiation strategy. The buyer should review options with their real estate agent and lender before making a decision.

What should buyers avoid during underwriting?

Buyers should avoid making large purchases, opening new credit accounts, changing jobs, moving money without documentation, or taking on new debt unless they have discussed it with their lender first. Even small financial changes can create new questions for underwriting.

Why does the lender ask for the same document more than once?

Sometimes a document has to be updated, clarified, reformatted, or reviewed by a different part of the lending team. It can feel repetitive, but those requests are often part of verifying the file before final approval.

What does “conditional approval” mean?

Conditional approval generally means the loan has moved forward, but certain items still need to be reviewed, updated, or cleared before closing. The conditions may involve income, assets, insurance, title, appraisal, or other loan-related documentation.

Can a loan still be denied during underwriting?

Yes, it is possible for a loan to be denied if the buyer no longer meets lender requirements or if issues arise with documentation, credit, employment, assets, appraisal, or property eligibility. This is why buyers should stay in close communication with their lender until closing is complete.

How can buyers make underwriting go more smoothly?

Buyers can help by responding quickly, sending complete documents, avoiding unexplained financial changes, and asking questions when they do not understand a request. Clear communication can reduce delays and prevent small issues from becoming larger ones.

Continue the Buyer Journey

Previously:

👉The Option Period Explained

Next:

As financing and appraisal milestones fall into place, the transaction moves toward its final stretch. The next post covers how to navigate closing week with less stress, better preparation, and fewer last-minute surprises.

Making Informed Buying Decisions Across North Texas & DFW

If you are planning to buy a home in Sachse, Princeton, Allen, or anywhere across North Texas and the DFW area, Cindy Coggins Realty Group can help you evaluate your options, understand how local market conditions may affect your decisions, and move forward with greater clarity at every stage of the process.

When you are ready, reach out to start the conversation and move forward with confidence.

Message Cindy to receive your complete copy of the Buyer’s Reality Check Series and buy with clarity instead of guesswork.

📞

Call or Text:

(469) 499-7452

📧

Email:

cindycoggins@kw.com

⭐

See why so many clients trust us—check out our 5-star reviews on Google.

Disclaimer:

This series is provided for general educational purposes only and is not intended as legal, financial, tax, lending, inspection, insurance, or real estate advice. Every buyer’s situation is different, and market conditions, loan requirements, contract terms, property conditions, timelines, and transaction decisions can vary. Readers should verify information independently and consult the appropriate professionals, including a real estate agent, lender, inspector, insurance provider, title company, attorney, CPA, and other qualified advisors as needed. Information is deemed reliable but not guaranteed.

Search Post

Recent Post